The Federal Reserve is not a part of the federal government, nor is it controlled by the federal

government. There is no Congressional oversight, no audits are performed, and, as of 1983, we do not even

know who owns the controlling interest. Yet, since 1913, the Federal Reserve controls our monetary system,

and we give them the right to create "new" money, and pay them interest on it.

THE GRACE REPORT

When Ronald Reagan took office, he commissioned a blue ribbon panel of businessmen to assess various

functions of the government, headed by Peter Grace.

This is a quote from that report:

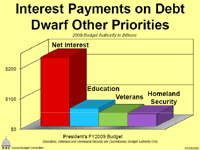

"100% of what is collected is absorbed solely by the interest on the Federal debt and by Federal Government contributions to transfer payments.

In other words, all individual income tax revenues are gone before one nickel is spent on the services which taxpayers expect from their Government."

Income tax revenues amount to around 20% to 25% of the revenue collected by the government. Other funds come from corporate income taxes, imports, cigarettes, gasolene and a slew of excise and other taxes. Further corruption of your tax dollar occurs when the Federal Reserve "loans" money to the government. These "loans" are simply Congress allowing the Reserve to print (spell that "create") money for the government to use. The bankers print these notes, with no value behind them ("fiat currency") , then send us the bill for the interest. Make sense? If so, please re-read the sentence. Due to the fact hat the money has no value behind it, the dollar is degraded and inflation is the result.

MONETIZATION

When the expenses of the U.S. Government exceed the revenue collected, it issues new debt to cover

the deficit. This debt typically takes the form of new issues of government bonds which are sold on

the open market. However, the debt can also be monetized* by which the Federal Reserve creates an

entry on its books to credit the US Government for an amount equal to the dollar amount of the bonds

the Federal Reserve is acquiring. The money created in this process not only includes the new

dollars that came into existence just to purchase the bonds, but much more because this new money is

now sitting in the form of checkbook money at the Federal Reserve.

Under the scheme of Fractional Reserve Banking** this new checkbook money is treated as an asset to lend against. The expansion of the money supply becomes many times the amount of the initial money created, with the exact amount being a function of what percentage of deposits banks must set aside as "reserves". By this system, $100.00 in fiat currency can become $10,000.00 in loans processed to consumers.

* Monetization is the process of converting or establishing something into legal tender. It usually refers to the printing of banknotes by central banks.

Debt monetization occurs when the Federal Reserve buys government bonds. Debt monetization prevents the government from taking capital out of the private market. Since there is a limited amount of capital available in the market, there will be less available to fund business growth if the government takes a substantial portion.

Debt monetization can be seen as a flat tax because the government acquires additional funds while the currency decreases in value.

In some industry sectors, monetization is a buzzword for adapting non-revenue-generating assets into those that generate revenue.

The ultimate consequence of monetizing U.S. debt is that it expands the money supply which will tend to dilute the value of dollars already in circulation. This is the cause of inflation.

** The Federal Reserve defines Fractional Reserve Banking thus: "The fact that banks are required to keep on hand only a fraction of the funds deposited with them is a function of the banking business. Banks borrow funds from their depositors (those with savings) and in turn lend those funds to the banks borrowers (those in need of funds). Banks make money by charging borrowers more for a loan (a higher percentage interest rate) than is paid to depositors for use of their money. If banks did not lend out their available funds after meeting their reserve requirements, depositors might have to pay banks to provide safekeeping services for their money. For the economy and the banking system as a whole, the practice of keeping only a fraction of deposits on hand has an important cumulative effect. Referred to as the fractional reserve system, it permits the banking system to create money."